IT14 Contributed Tax Capital

Detailed below is the screen that you are required to fill in for contributed tax capital. The list is only a requirement for medium large companies and it is necessary to do one for each type of share class that the company has. Contributed Tax Capital is a concept that the preparers of tax returns should be familiar with.

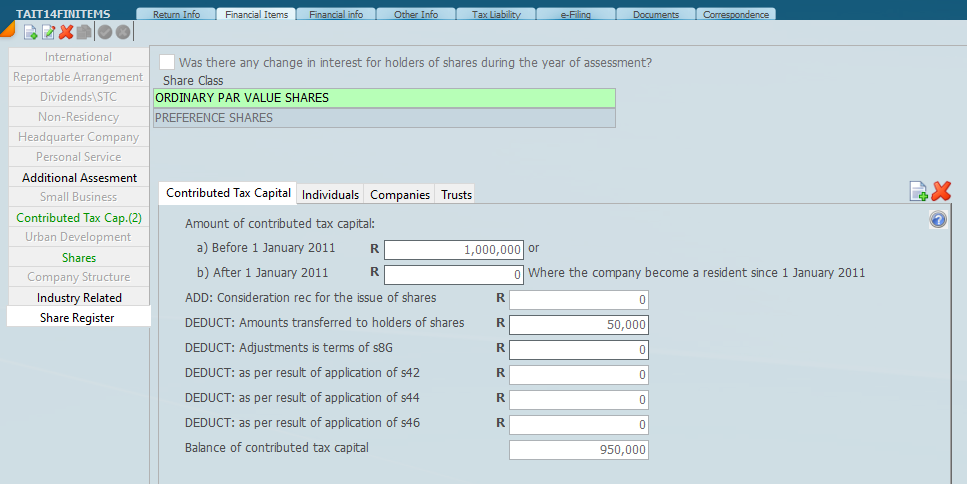

Enter the Contributed Tax Capital on the screen below. To enter the data click on the Share Register you want to work with. Select edit and the fields will be in yellow.

## Contributed tax capital (CTC) – what it is

“Contributed tax capital” (CTC) is a tax concept defined in section 1 of the Income Tax Act, and it is determined *separately for each class of shares* in a company. In simple terms, it represents the tax-recognised share capital contributed by shareholders for that class of shares, reduced by amounts that the company has already returned to shareholders as CTC.

### How CTC is built up (high level)

For most companies (i.e. “any other company” in the definition), CTC for a class of shares is broadly the total of:

* the company’s stated capital / share capital and share premium relating to that class of shares immediately before 1 January 2011 (with an adjustment for amounts that would have been “dividends” under the pre‑2011 definition), plus

* the consideration received by or accrued to the company for the issue of shares of that class on or after 1 January 2011, plus

* where shares were converted from another class, certain amounts relating to that conversion,

less amounts that the company has transferred for the benefit of shareholders in respect of that class of shares (i.e. amounts returned out of CTC), subject to conditions.

There are also specific rules for a foreign company that becomes a South African tax resident, where CTC starts (in part) with the market value of the shares immediately before it becomes resident, plus later share issue consideration, reduced by transfers for the benefit of shareholders.

### Important “fairness” conditions when returning CTC

The definition contains safeguards. For example, a transfer of CTC must generally be pro‑rata within the class (equal CTC per share and not exceeding the available CTC per share).

## Why CTC matters (dividend vs return of capital)

CTC is crucial because it draws the line between:

* a dividend (taxed under the dividends tax system), and

* a return of capital (a repayment of contributed capital).

The Income Tax Act definition of “dividend” specifically excludes any amount transferred/applied to the extent that it results in a reduction of the company’s CTC.

A “return of capital” is defined as an amount transferred by a resident company in respect of a share to the extent that it results in a reduction of CTC, whether paid as a distribution or as consideration for the acquisition of a share.

## Other points

* If amounts relevant to CTC are in a foreign currency, section 25E requires translation using the spot rate on the relevant date.

* There are additional specific rules dealing with CTC in certain group/company transactions (for example, section 8G).

12 May 2026