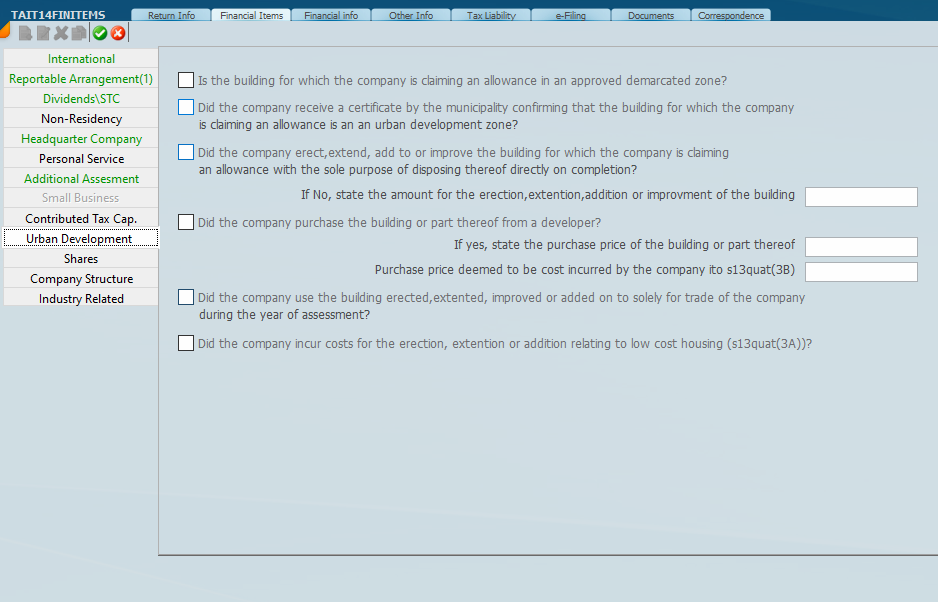

On the main screen if Urban Development is ticked this screen will be available for entry.

The Income Tax Act contains a specific incentive commonly referred to as an “Urban Development Zone (UDZ) claim” – the allowance in section 13quat for the erection or improvement of buildings in urban development zones .

## 1) What the UDZ “urban development” claim is

Section 13quat(2) allows an allowance (deduction) from income in respect of the cost of the erection, extension, addition or improvement of a commercial or residential building (or part) that:

- is owned by the taxpayer and

- is used solely for the purposes of that taxpayer’s trade, and

- is situated within an urban development zone .

An “urban development zone” is an area demarcated by a municipality under the Act and published in the Gazette .

## 2) Key qualifying requirements (high level)

A UDZ allowance is available only if (amongst other requirements):

- The building is situated within an urban development zone .

- The erection/improvement was commenced on or after the relevant Gazette notice date for that UDZ and in terms of a contract formally and finally signed on/after that date .

- The work covers the entire building or at least 1,000 m² floor area .

- If purchased from a developer, additional conditions apply (including that the developer did not claim the allowance and, in certain cases, improvement spend must be at least 20% of purchase price) .

## 3) What “cost” includes/excludes

For section 13quat, “cost” generally means costs actually incurred excluding borrowing/finance costs, and can include demolition, excavation, and certain directly adjoining works (water/power/parking, drainage/security, waste disposal, access/frontage) .

## 4) The allowance percentages (how the deduction is calculated)

Section 13quat(3) provides (summary):

- New building / extension / addition: 20% in the year the building is brought into use, plus 8% in each of the 10 succeeding years .

- Improvement of an existing building where the structural/exterior framework is preserved: 20% in the year brought into use, plus 20% in each of the 4 succeeding years .

For low-cost residential units, section 13quat(3A) provides different rates (including 25% / 13% / 10% for new/extended/additional low-cost units, and 25% + 25% for 3 years for low-cost improvements) .

## 5) Documentation/certificates you must have

No deduction is allowed unless the taxpayer has the required information for submission to SARS, including (notably) a municipal certificate confirming the building is located within a UDZ, and cost particulars (and, where relevant, developer certificates) .

The SARS trust return guide also reflects these UDZ questions (demarcated zone confirmation, municipal certificate, whether erected/improved, purchase from developer, etc.) .

## 6) Timing/sunset date (important)

A deduction under section 13quat is not allowed for a building/improvement brought into use after 31 March 2025 .

12 May 2026