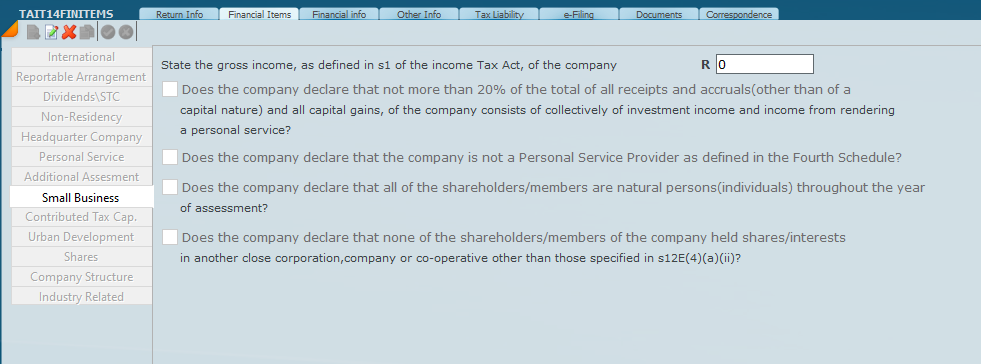

On the front page if the company has been indicated as a small business it will be necessary to complete the screen shown below in order to get the small business rates.

Please be aware of the provisional tax calculation to insure that the calculation is on small business.

In South Africa there are two main “small business” income tax regimes that people often mean when they say “small business tax”, each with its own specialised tax table:

1) Small Business Corporation (SBC) regime – section 12E of the Income Tax Act (a *company/CC/co-op* regime with *progressive* tax rates and accelerated depreciation).

2) Turnover Tax for micro businesses – Sixth Schedule read with sections 48A–48C of the Income Tax Act (a simplified tax on *turnover*, not taxable income).

## 1) Small Business Corporation (SBC) – how it works (section 12E)

### (a) Who can qualify (typical requirements)

A company/CC/co-operative must meet the section 12E requirements. Key practical requirements include:

* Gross income limit: must not exceed R20 million for the year of assessment.

* Shareholders/members: must be natural persons, and generally may not hold shares in other private companies (subject to specific permitted exceptions).

* Nature of income: not more than 20% of the SBC’s gross income and capital gains may come from investment income and/or personal service income.

* Personal service / professional services exclusion: entities rendering listed “personal services” (for example consulting, accounting, legal, medical, IT etc.) are generally excluded unless they employ at least three full-time employees who are not shareholders/members.

### (b) What the benefit is

If you qualify, you get:

* Concessionary (progressive) corporate income tax rates (instead of the flat company rate).

* Accelerated depreciation / wear-and-tear allowances on qualifying assets, for example:

* Plant and machinery used in manufacturing: 100% in the year acquired and brought into use; and

* Other depreciable assets: generally 50% / 30% / 20% over three years.

### (c) The specialised SBC tax tables (examples from the SARS tax tables in the knowledge)

These tables are applied to the company’s taxable income (not turnover), if it qualifies as an SBC.

Years of assessment ending from 1 April 2026 to 31 March 2027 (SBC rates)

| Taxable income | Rate of tax |

|---|---|

| 1 – 99 000 | 0% |

| 99 001 – 365 000 | 7% of amount above 99 000 |

| 365 001 – 550 000 | 18 620 + 21% of amount above 365 000 |

| 550 001 and above | 57 470 + 27% of amount above 550 000 |

Sky does not do Turnover Tax

## 2) Turnover Tax for “registered micro businesses” – how it works (Sixth Schedule)

### (a) What it is

This is a separate system called turnover tax, imposed by section 48A, payable by a person that is a registered micro business, on its taxable turnover for that year (not “taxable income”).

The Act also contains transitional rules dealing with amounts received/accrued when entering/leaving the micro business regime (section 48C).

### (b) The specialised turnover tax tables (examples in the knowledge)

Years of assessment commencing on or after 1 March 2023 (registered micro business turnover tax table)

| Taxable turnover | Rate of tax |

|---|---|

| Not exceeding R335 000 | 0% |

| R335 001 – R500 000 | 1% of amount above R335 000 |

| R500 001 – R750 000 | R1 650 + 2% of amount above R500 000 |

| Above R750 000 | R6 650 + 3% of amount above R750 000 |

Turnover tax table for 1 March 2026 to 28 Feb 2027 / company years ending 1 April 2026 to 31 March 2027

| Taxable turnover | Rate of tax |

|---|---|

| 1 – 600 000 | 0% |

| 600 001 – 950 000 | 1% of amount above 600 000 |

| 950 001 – 1 400 000 | 3 500 + 2% of amount above 950 000 |

| 1 400 001 and above | 12 500 + 3% of amount above 1 400 000 |

---

## 3) Practical way to think about “small business tax”

* If you operate through a company/CC and meet the section 12E requirements, the SBC regime taxes you on taxable income using the SBC progressive table, and you may get accelerated depreciation.

* If you qualify and register as a micro business, turnover tax is a simplified turnover-based calculation using the micro business turnover table.

12 May 2026