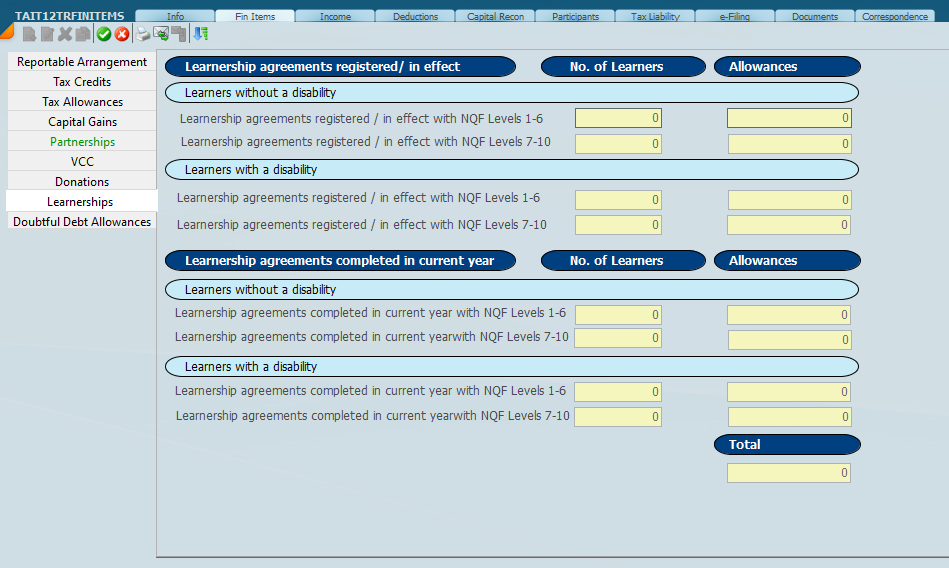

In edit mode enter the details of the learnerships.

A trust can claim the learnership allowance under section 12H of the Income Tax Act where the trust qualifies as the “employer” party to a registered learnership agreement entered into pursuant to a trade carried on by that employer. The trust tax return (ITR12T) specifically includes a container to calculate the section 12H learnership allowance.

### 1) What qualifies (overview)

- A “registered learnership agreement” is a learnership agreement that is registered in accordance with the Skills Development Act, 1998 and is entered into between a learner and an employer before 1 April 2027.

- The deduction is allowed where the agreement is entered into pursuant to a trade carried on by the employer.

### 2) Amounts of the allowance (agreements entered on/after 1 October 2016)

The trust return guide reflects the standard amounts to be used in calculating the deduction:

- Without a disability

- NQF 1–6: R40,000

- NQF 7–10: R20,000

- With a disability

- NQF 1–6: R60,000

- NQF 7–10: R50,000

These amounts align with the Income Tax Act provisions (R40,000 for NQF 1–6 and R20,000 for NQF 7–10, with additional increases where the learner has a disability).

### 3) Pro-rating for part-year learnerships

If the learner is party to the registered learnership agreement for less than 12 full months during the relevant year of assessment, the allowance is apportioned based on full months (ratio of months/12).

### 4) Additional allowance on completion (where the learner successfully completes)

The Act provides additional deductions where the learner successfully completes the learnership during the year of assessment, including where the agreement duration is:

- Less than 24 full months (completion allowance), and

- 24 full months or more, where the R40,000 or R20,000 is multiplied by the number of consecutive 12-month periods within the duration of the agreement.

### 5) Disability uplift (increase)

Where the learner is a person with a disability at the time of entering into the learnership agreement, the allowance amounts are increased:

- For certain subsections, by R20,000, and

- For other subsections, by R30,000.

### 6) Anti-abuse limitation

Section 12H does not apply where:

- The learner previously failed to complete another registered learnership agreement involving the employer (or an associated institution), and

- The new agreement contains the same education and training component as that other agreement.

### 7) Reporting / information obligations (SETA)

The Act provides that:

- The SETA must submit information to the Minister as required, and

- In each year an employer is eligible for the deduction, the employer must submit information to the SETA as required by the SETA.

### 8) Sunset date (important)

The trust return guide notes the sunset date was extended (from 1 April 2024) to 31 March 2027 for purposes of the learnership incentive reflected in the return.

12 May 2026