ITR12 Trust Doubtful Debts

In edit mode enter the details required about doubtful debts.

A trust can claim a doubtful debt allowance under section 11(j) of the Income Tax Act</strong>, provided the “debt due to the taxpayer” (the trust) is of a nature that <strong>would have been deductible if it became bad. (If a debt actually becomes bad, section <strong>11(i)> provides for a bad debt deduction, subject to the requirement that the amount was included in income in the current or prior year(s) .

## 1) Doubtful debt allowance – how section 11(j) works (trusts included)

Section 11(j) distinguishes between whether IFRS 9 is applied to the debt for financial reporting purposes:

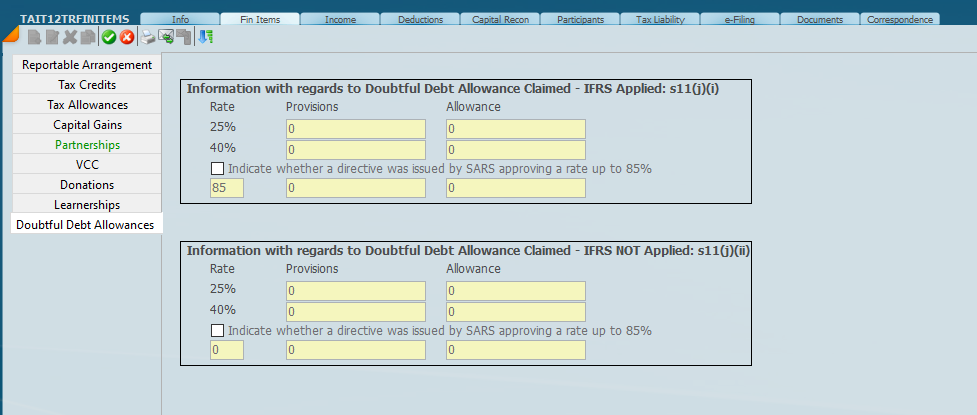

### (a) IFRS 9 applied (s11(j)(i))

The allowance is broadly calculated using <strong>40%</strong> and <strong>25% components based on IFRS 9 impairment (expected credit loss) amounts, including certain bad debts written off for accounting purposes that have not previously been allowed as a deduction .

### (b) IFRS 9 not applied (s11(j)(ii))

The allowance is based on how long the debt is overdue (after taking account of security):

* 40%</strong> of qualifying debts that are <strong>120 days or more in arrears

* 25%</strong> of qualifying debts that are <strong>60 days or more in arrears (but not already included in the 120+ day category)

### (c) Recoupment / reversal in the following year

Section 11(j) provides that an allowance under this paragraph must be included in income in the following year of assessment</strong>

### (d) SARS directive up to 85%

The Act also indicates the Commissioner may issue a directive to increase the percentage (up to <strong>85%</strong>) after considering factors like repayment history and enforcement steps.

## 2) SARS trust return guidance (ITR12T) – where it appears for trusts

SARS’s Comprehensive Guide to the Income Tax Return for Trusts specifically includes

* “Bad/Doubtful debts” as an expense line item in the trust’s business/trading income section

* Specific fields for the doubtful debt allowance in the return:

* “Doubtful debt allowance – IFRS applied (s11(j)(i))” and

* “Doubtful debt allowance – IFRS not applied (s11(j)(ii)) .

* Where a value is entered, the return requires supporting detail at the <strong>25% and 40% rates</strong>, and also asks whether a <strong>directive for an 85% rate was issued .

12 May 2026