IT14 Reportable Arrangement

On the main screen if Reportable Arrangement is ticked this screen will be available for entry.

A reportable arrangement is defined in the Tax Administration Act as an “arrangement” referred to in section 35(1) or listed in a public notice under section 35(2), that is *not* an excluded arrangement under section 36 .

### Key related definitions (TAA s34)

- “Arrangement” means any transaction, operation, scheme, agreement or understanding (whether enforceable or not) .

- A “participant” includes a promoter, a person who will derive (or assumes they will derive) a tax benefit or financial benefit from the arrangement, or any other person party to an arrangement listed by public notice .

- “Tax benefit” means the avoidance, postponement, reduction or evasion of a liability for tax .

- “Promoter” is a person principally responsible for organising, designing, selling, financing or managing the arrangement .

### When an arrangement becomes “reportable” (TAA s35)

An arrangement is reportable if a person is a participant and the arrangement meets any of these triggers, including where it—

- has charges (interest/finance costs/fees) dependent on assumptions about the tax treatment of the arrangement ;

- has characteristics contemplated in Income Tax Act s80C(2)(b) (or substantially similar characteristics) ;

- creates a mismatch between tax and accounting treatment (e.g., a tax deduction but not an accounting expense, or accounting revenue but not gross income for tax) ;

- does not result in a reasonable expectation of pre-tax profit for any participant ; or

- results in an expected pre-tax profit less than the present value of the tax benefit .

It is also reportable if the Commissioner lists the arrangement in a public notice .

### Excluded arrangements (TAA s36) – not reportable (unless structured mainly for a tax benefit)

Certain common transactions are excluded (subject to conditions), including: certain plain-vanilla debts, leases, exchange-regulated transactions, and participatory interests in regulated collective investment schemes .

### Disclosure requirement (TAA s37–39)

If it is a reportable arrangement, the prescribed information must generally be disclosed within 45 business days , and SARS then issues a reportable arrangement reference number .

Under the Tax Administration Act, an arrangement becomes a reportable arrangement if it meets one of the triggers in TAA s35(1) (or is listed by the Commissioner in a public notice under s35(2)) . Practical examples (by category) include:

1) “Round trip financing” type arrangements

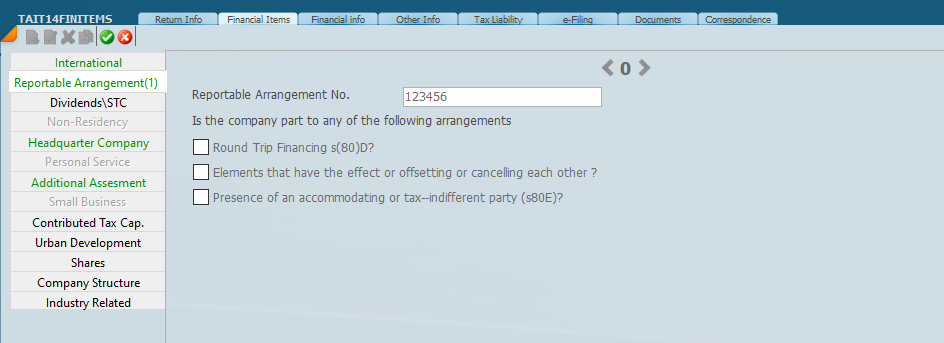

These are arrangements where funds are transferred between/among parties, the transfers would result (directly or indirectly) in a tax benefit, and they significantly reduce/offset/eliminate business risk .

Because round trip financing is listed as a characteristic indicative of a lack of commercial substance in Income Tax Act s80C(2)(b) , and TAA s35 includes arrangements with characteristics contemplated in s80C(2)(b) , these can be reportable.

2) Arrangements involving an “accommodating” or “tax-indifferent” party

These involve a party where amounts derived are not subject to normal tax or are significantly offset by expenditure/losses, and their participation causes tax-character changes (for example revenue/capital shifts, deductions created, income not included or exempt, etc.) .

This is also a characteristic listed under ITA s80C(2)(b) and therefore can trigger reportability under TAA s35(1)(b) .

3) Arrangements with “offsetting or cancelling” elements

Where the scheme includes elements that have the effect of offsetting or cancelling each other, that feature is specifically listed as indicative of lack of commercial substance under ITA s80C(2)(b) , and can therefore be reportable under TAA s35(1)(b) .

SARS’s trust return guide even flags these as reportable-arrangement type features (along with round-trip financing and accommodating/tax-indifferent parties) .

4) Tax/accounting mismatch arrangements

For example, arrangements that give rise to amounts disclosed as:

- a deduction for Income Tax purposes but not an expense under financial reporting standards; or

- revenue under financial reporting standards but not “gross income” for Income Tax .

These are expressly listed in TAA s35(1)(c) .

5) Arrangements with little or no real economic profit (compared to the tax benefit)

Examples include arrangements that:

- do not result in a reasonable expectation of pre-tax profit for any participant; or

- have expected pre-tax profit less than the value of the tax benefit (discounted to present value) .

6) Arrangements where finance charges depend on assumed tax treatment

For example, where the calculation of interest/finance costs/fees/charges is wholly or partly dependent on assumptions about the tax treatment of the arrangement .

7) Any arrangement SARS lists by public notice

Even if it doesn’t obviously fall into the categories above, an arrangement is reportable if the Commissioner lists it in a public notice .

11 May 2026