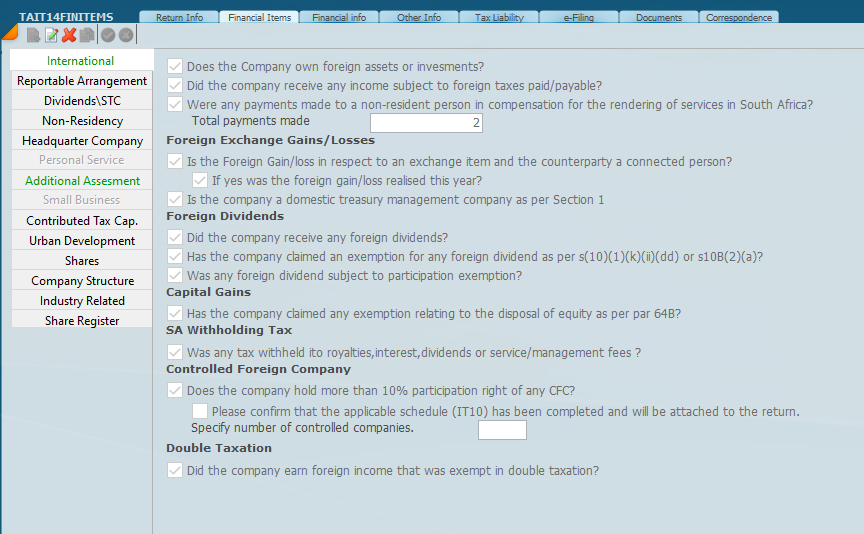

On the main screen if International is ticked this screen will be available for entry. This screen queries if there are dealings with foreign entities as indicated on the screen below. If the answer to any of the questions of the items listed is yes ensure that you tick the correct item. A mistake on this screen can be taken as misrepresentation.

The International Section of the ITR14 — A Plain-English Walkthrough of the Law

South Africa moved from a source-based to a residence-based tax system on 1 January 2001. The consequence is simple but far-reaching: a South African resident company is taxed on its worldwide income, not just what it earns inside the Republic. The "International" section of the ITR14 is essentially SARS's filter to figure out which parts of the Income Tax Act 58 of 1962 ("the Act") need to be applied to your company. Each question on that screen maps directly to a provision (or a cluster of provisions) of the Act. Let me work through them in the order they appear.

Foreign assets and foreign income — the opening three questions

"Does the Company own foreign assets or investments?" This is the residence-based net being cast. If a resident company holds foreign shares, foreign immovable property, foreign bank accounts, foreign loan receivables, etc., several consequences follow:

-

Foreign-source income (interest, rentals, royalties) must be included in gross income under section 1's definition.

-

Any disposal of foreign assets falls within the Eighth Schedule (capital gains tax) on a worldwide basis.

-

Foreign assets feed into the participation exemption analysis, CFC analysis, and ringfencing of foreign assessed losses under section 20A and section 20B.

"Did the company receive any income subject to foreign taxes paid/payable?" This question triggers section 6quat, the foreign tax credit ("rebate") regime. Because the company is taxed in SA on its worldwide income, it would otherwise be double-taxed where a foreign country has already taxed the same income at source. Section 6quat(1) gives a rebate (a credit against SA tax) for foreign taxes on foreign-sourced income. Section 6quat(1C) gives a deduction (not a rebate) for foreign taxes on SA-sourced trade income that another country has nonetheless taxed. The rebate is limited to the SA tax that would have been payable on that foreign income — you can't use excess foreign credits to shelter purely SA-source income.

"Were any payments made to a non-resident person in compensation for the rendering of services in South Africa?" This is a flag for two things. First, section 23(o) prohibits a deduction for bribes or for fines/penalties for unlawful activities — not directly the point here, but related to payments crossing the border. Second, and more relevant, this disclosure helps SARS test whether the non-resident was conducting business through a permanent establishment under a double tax agreement (DTA), and whether PAYE should have been withheld on services rendered physically in South Africa. Non-resident service providers can be taxable in SA on SA-source service income, with relief usually only available through a DTA.

Foreign Exchange Gains/Losses

The two questions here are about section 24I, which governs the taxation of foreign exchange differences on "exchange items" (foreign currency debts, loans, forward exchange contracts, foreign currency options). The key issue flagged is whether the counterparty is a connected person. This matters because section 24I(10) and (10A) contain deferral rules: where the exchange item is between connected persons (or between a CFC and a connected resident), the unrealised gain or loss is deferred until realisation rather than being taxed annually on a mark-to-market basis. This prevents groups from manufacturing artificial timing differences on intra-group foreign loans.

The "domestic treasury management company" question relates to section 1's definition and the special exchange-control and tax dispensation for treasury companies registered with the South African Reserve Bank to manage offshore subsidiaries' cash for SA multinationals.

Foreign Dividends

A "foreign dividend" is defined in section 1(1) and is included in gross income. It is then potentially exempted under section 10B:

-

Section 10B(2)(a) — the participation exemption. A foreign dividend is fully exempt if the SA recipient (alone or with group companies) holds at least 10% of the equity shares and voting rights in the foreign company declaring the dividend. This recognises that the foreign profits have already borne foreign corporate tax, and rewards genuine substantial holdings.

-

Section 10B(2)(b) — country-to-country exemption. A foreign dividend paid by a foreign company to a foreign company resident in the same country is exempt — relevant where a CFC receives a dividend from a sister CFC in the same jurisdiction.

-

Section 10(1)(k)(ii)(dd) — referenced in the form alongside section 10B(2)(a) — deals with the interaction between foreign dividends and the dividends tax / income tax exemption regime, particularly preventing double exemption.

Where no exemption applies, the foreign dividend is taxed under section 10B(3) at an effective rate, achieved by exempting a fraction (currently 17/27 for companies) so that the remainder taxed at 27% gives roughly a 10% effective rate, matching the dividends tax rate.

Capital Gains — Participation Exemption on Disposal

The question on the form points to paragraph 64B of the Eighth Schedule. This is the capital-gains-tax twin of section 10B(2)(a). If a resident disposes of equity shares in a foreign company to a non-resident, and the seller held at least 10% of the equity shares and voting rights for at least 18 months before disposal, the capital gain (or loss) is disregarded. The policy reasoning is that the retained earnings underlying the share value would have qualified for the foreign dividend participation exemption had they been declared instead — so the gain on disposal gets parallel treatment.

SA Withholding Taxes

The question "Was any tax withheld ito royalties, interest, dividends or service/management fees?" covers the suite of South African withholding taxes payable when a resident pays certain amounts to non-residents:

-

Dividends tax (section 64E onwards) — 20% on dividends paid to non-residents, reduced by DTAs (often to 5%, 10% or 15%).

-

Withholding tax on interest (sections 50A–50H) — 15% on SA-source interest paid to non-residents, with various exemptions (e.g. listed debt, certain bank deposits) and DTA reductions.

-

Withholding tax on royalties (sections 49A–49E) — 15% on royalties paid to non-residents, again subject to DTAs.

-

The "service/management fees" reference is historical — a withholding tax on service fees was legislated in sections 51A–51H but repealed before it ever came into effect. The question lingers, but no withholding currently applies to pure service fees (subject of course to PAYE if services are physically rendered in SA).

Controlled Foreign Company (CFC)

This is the most legally dense area on the form, governed by section 9D read with the IT10B schedule.

What is a CFC? Under section 9D(1), a foreign company is a CFC if more than 50% of its participation rights or voting rights are held directly or indirectly by one or more South African residents, or its financial results are consolidated (under IFRS 10) into a resident company's financials. Headquarter companies are excluded from this counting.

Why does the form ask about a 10% participation right? Because section 9D(2) imputes a proportional share of the CFC's "net income" into the resident shareholder's income — but only if that resident holds at least 10% of the participation rights. Below 10%, the resident is not subject to imputation. So the form is asking whether the company crosses the 10% imputation threshold; if yes, the IT10B schedule must be completed.

How does imputation work? Section 9D recalculates the CFC's income as if it were an SA taxpayer (applying SA rules, including the Eighth Schedule), and includes a pro-rata share in the resident shareholder's income. There are important exemptions:

-

Foreign Business Establishment (FBE) exemption — section 9D(9)(b): net income attributable to a genuine FBE (a fixed place of business, suitably staffed and equipped) is excluded from imputation. This is the exemption the Constitutional Court considered in Coronation Investment Management SA (Pty) Ltd v CSARS [2024] ZACC 11 in 2024, where the court found Coronation's Irish subsidiary qualified as an FBE despite outsourcing investment management functions.

-

High-tax exemption — section 9D(2A): if the foreign tax on the CFC's income is at least the prescribed proportion of the SA tax that would have been payable (the threshold has moved between 75% and lower percentages over the years — currently 67.5% per recent amendments), no imputation.

-

Diversionary/participation exemptions for foreign dividends within CFCs under section 9D(9)(f).

Number of controlled companies — the field on the form simply asks how many separate CFCs the company holds, because each one requires its own IT10B disclosure.

Headquarter Company (visible in the left-hand sidebar)

A headquarter company under section 9I is a special vehicle to make South Africa attractive as a regional gateway into Africa. To qualify, broadly:

-

Each shareholder (alone or with the group) must hold at least 10% of the equity shares and voting rights;

-

At least 80% (by cost) of the company's assets must be in qualifying foreign holdings (10%+ shareholdings in foreign companies, or loans to / IP licensed to such foreign companies); and

-

If gross income exceeds R5 million, at least 50% must come from such qualifying foreign sources.

A headquarter company is excluded from CFC counting (so its foreign subsidiaries aren't dragged into SA's CFC net through it), is exempt from dividends tax on dividends paid out, and gets relief from interest and royalty withholding taxes on flow-through payments.

Double Taxation

"Did the company earn foreign income that was exempt in double taxation?" This asks whether the company has foreign income that is exempted from SA tax by virtue of a Double Tax Agreement (rather than by section 10B or 9D exemptions). DTAs override domestic law where they conflict, by virtue of section 108 of the Income Tax Act read with section 231 of the Constitution. A typical example: business profits earned by an SA company through a permanent establishment in a treaty country, where the treaty allocates exclusive taxing rights to that other country, are exempt in SA — although SA usually retains the right to tax (with credit) rather than fully exempt, depending on the treaty.

A few practical pointers

The reason SARS asks all of these as "Yes/No" gatekeeping questions is that each "Yes" expands the ITR14 to add the relevant schedules and disclosure containers. Practically, getting these wrong is a common audit trigger:

-

Answering "No" to the foreign assets question when the company holds a foreign bank account or foreign shares is a misrepresentation under section 234 of the Tax Administration Act.

-

Not declaring CFC holdings exposes the company to the imputation amount plus understatement penalties under Chapter 16 of the TAA (up to 200% in cases of intentional tax evasion).

-

The participation exemptions in section 10B(2)(a) and paragraph 64B both require careful share-counting — particularly because "equity shares" excludes shares with capped participation rights, so preference shares often don't count.

If you want, I can dig deeper into any specific question — for example the CFC net income calculation in section 9D, the section 6quat rebate mechanics, or how DTAs interact with the participation exemption.

11 May 2026