On the main screen if Headquarter is ticked this screen will be available for entry.

A “headquarter company” (often called an HQ company) is an Income Tax Act concept.

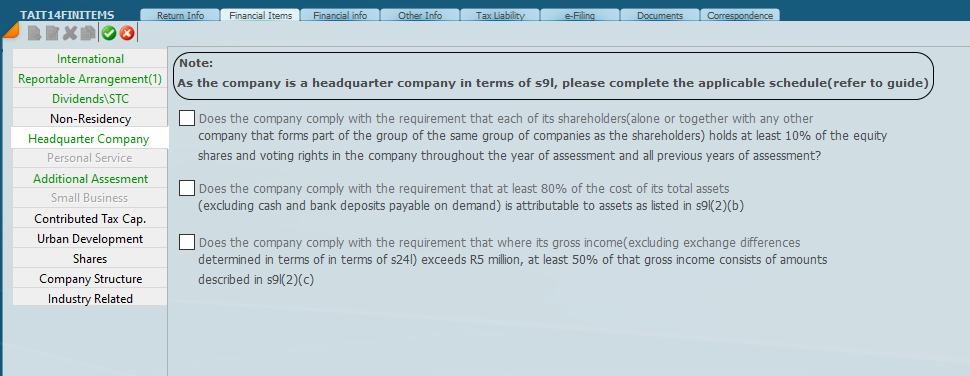

In terms of the definition in section 1 of the Income Tax Act, a “headquarter company” in respect of any year of assessment means a company contemplated in section 9I(1) in respect of which an election has been made in terms of that section .

### What section 9I requires (in summary)

Under section 9I(1), a company may elect (in the form and manner determined by the Commissioner) to be a headquarter company for a year of assessment if it:

- is a resident; and

- complies with the requirements in section 9I(2) .

Under section 9I(2) (as shown in the Act extract), the key requirements include, broadly:

1) Shareholding / control requirement (10% holders)

For the duration of that year of assessment, each holder of shares in the company (alone or together with its group companies) must hold at least 10% of the equity shares and voting rights in the company .

At the end of that year (and all previous years), 80% or more of the cost of the company’s total assets must be attributable to qualifying interests in relation to foreign companies in which the HQ company (alone or together with its group companies) holds at least 10% of the equity shares and voting rights (including interests in equity shares, debt owed by, or qualifying intellectual property licensed to those foreign companies) .

Certain cash / bank deposits payable on demand are excluded when determining “total assets”, and the provision includes a limitation where the company did not own assets exceeding R50 000 market value during a year .