IT14 Additional Assessment

On the main screen if a number of items are ticked the following screens will be avialable for entry.

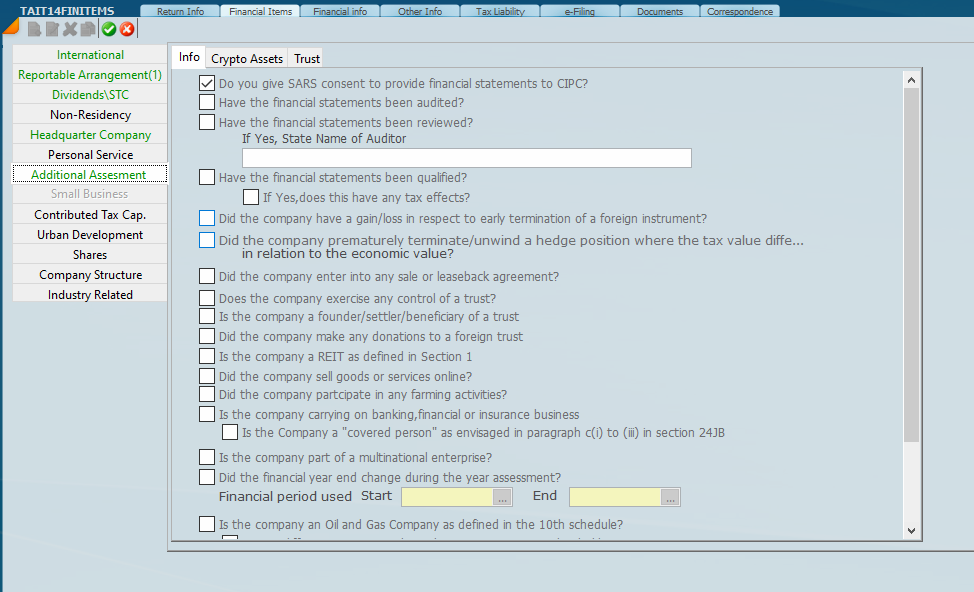

The "Info" Tab of the ITR14 — Tick-Box Walkthrough

This screen is part of SARS's customisation engine. Each tick expands the return with additional disclosure containers and engages specific provisions of the Income Tax Act 58 of 1962 ("the Act"), the Tax Administration Act 28 of 2011 ("TAA") and, in some cases, the Companies Act 71 of 2008. Working top to bottom:

Financial statement disclosures

"Do you give SARS consent to provide financial statements to CIPC?" This is an administrative consent under the Promotion of Access to Information Act and the SARS confidentiality provisions in section 69 of the TAA. SARS may not ordinarily share taxpayer information with another organ of state (here, the Companies and Intellectual Property Commission). By consenting, the company waives this protection so that SARS can hand the AFS over to CIPC, which is meant to streamline annual-return compliance under section 33 of the Companies Act. There is no direct tax consequence — it's an information-sharing election.

"Have the financial statements been audited?" / "reviewed?" / "qualified?" / "If Yes, does this have any tax effects?" Audit and review requirements come from section 30 of the Companies Act and Regulation 28 of the Companies Regulations 2011, which use a "public interest score" to determine whether AFS must be audited, independently reviewed, or merely compiled. From a tax angle, the disclosure matters because:

-

Audited AFS carry significantly more evidential weight in any SARS verification or audit under section 40 of the TAA. SARS' burden of proof to disturb audited figures is practically higher.

-

A qualified audit opinion is a red flag that the financial figures used as the starting point for the tax computation may be unreliable. SARS will scrutinise whether the matter giving rise to the qualification has tax consequences (e.g. unverified inventory, going-concern doubt affecting deferred tax, unsupported provisions).

-

Section 99 of the TAA sets prescription periods — three years for assessments, but extended where there has been fraud, misrepresentation, or non-disclosure of material facts. A qualification can be evidence of such non-disclosure.

Foreign instruments and hedging

"Did the company have a gain/loss in respect to early termination of a foreign instrument?" This engages section 24I (exchange differences) and section 24J (incurral and accrual of interest). Early termination of a foreign-currency instrument crystallises previously unrealised exchange differences and breaks the symmetry of the accrual basis. If the instrument is between connected persons, the deferral rules in section 24I(10) / (10A) fall away on termination and the deferred gain or loss comes home to roost in one bite.

"Did the company prematurely terminate/unwind a hedge position where the tax value differs in relation to the economic value?" This is targeting tax-economic mismatches on hedges. South African tax law generally taxes financial instruments under sections 24I, 24J, 24JA (Sharia-compliant), 24JB (covered persons) and 24O (acquisition-debt interest), but the timing and character can diverge from IFRS hedge accounting. When a hedge is unwound early, the "tax value" (cumulative gains/losses already brought to tax) can sit out of line with the "economic value" (the real cash position). SARS asks because unwinds are a classic vehicle for crystallising capital losses on the tax side while the economic gain sits on the hedged item — which can engage the general anti-avoidance rule (GAAR) in sections 80A–80L of the Act.

Sale and leaseback

"Did the company enter into any sale or leaseback agreement?" Sale-and-leaseback transactions are governed by a tight cluster of anti-avoidance provisions because they were historically used to convert non-deductible capital expenditure into deductible rentals:

-

Section 23G restricts the deduction of rentals to the lessor's tax cost where the lessee originally owned the asset.

-

Section 23A ringfences capital allowances on lessor-owned assets to the income produced from those assets ("affected assets").

-

The wear-and-tear allowance under section 11(e) and section 12C for the lessor may also be affected.

-

If structured artificially, section 103 (now sections 80A–80L) GAAR can apply.

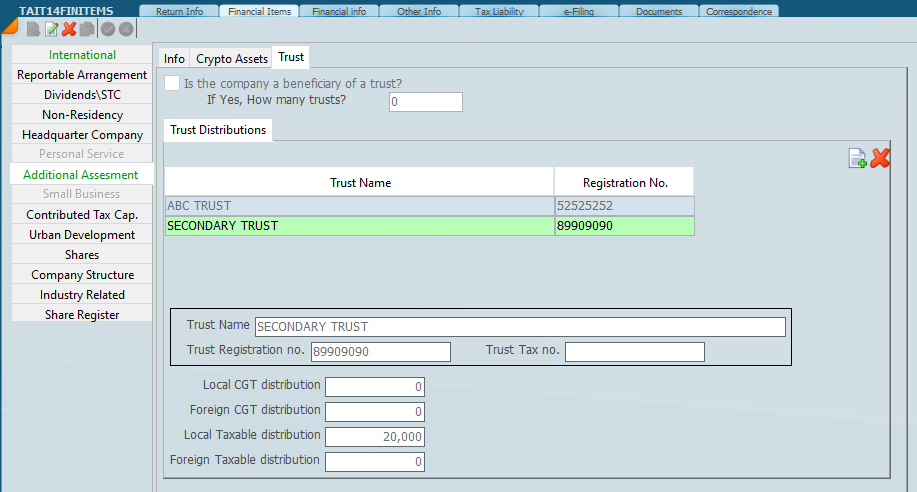

Trust connections

"Does the company exercise any control of a trust?" / "Is the company a founder/settler/beneficiary of a trust?" / "Did the company make any donations to a foreign trust?"

These three questions screen for trust-based tax exposures:

-

Section 7 (deemed accrual of income to a donor) attributes income of a trust back to the person who made a donation, settlement or other gratuitous disposition to the trust. Section 7(8) specifically catches resident donors who make donations to non-resident trusts, attributing the trust's income back to the SA donor.

-

Section 7C deals with interest-free or low-interest loans to trusts (including foreign trusts), deeming foregone interest to be a donation subject to donations tax at 20%/25% under section 54.

-

Paragraphs 68–72 of the Eighth Schedule are the CGT analogues, attributing capital gains of a trust back to the donor.

-

Donations to foreign trusts also trigger paragraph 80 of the Eighth Schedule considerations and may interact with the CFC rules in section 9D where the trust holds a foreign company.

Being a beneficiary matters because distributions of capital from a foreign trust to a resident beneficiary can be deemed income under section 25B(2A) to the extent they derive from foreign income that has not previously been taxed in SA, and capital gains distributed are attributed under paragraph 80(3) of the Eighth Schedule.

REITs

"Is the company a REIT as defined in Section 1?" A Real Estate Investment Trust is defined in section 1(1) by reference to the JSE Listings Requirements. REITs are taxed under a special flow-through regime in section 25BB, where:

-

"Qualifying distributions" paid out to shareholders are deductible to the REIT (s 25BB(2));

-

The deduction effectively shifts tax from the REIT to the unit-holder;

-

A REIT is exempt from CGT on disposal of immovable property and from dividends tax on qualifying distributions out (s 64F).

The question flips on the dedicated REIT schedule in the return.

E-commerce

"Did the company sell goods or services online?" The relevance is twofold. First, place-of-supply and VAT rules under the Value-Added Tax Act 89 of 1991 (in particular the electronic services regulations) — although VAT is captured elsewhere, SARS uses ITR14 disclosures to cross-check. Second, source of income under section 9, which has special rules for "place of effective management" and the location where contracts are concluded. Online sales raise live issues about whether a permanent establishment exists in SA (for non-residents) or in a foreign country (for SA residents trading abroad), which feeds back into the international section and section 6quat credits.

Farming

"Did the company participate in any farming activities?" Farming has its own tax regime in the First Schedule to the Act. Key features:

-

Paragraph 12 allows accelerated capital allowances for farming improvements (dams, fences, roads, machinery, plantations);

-

Paragraph 13 provides a rating formula to smooth volatile farming income;

-

Paragraph 8 governs the valuation of livestock and produce on hand, using standard values or actual cost;

-

Section 26 brings farming income into tax in accordance with the First Schedule. A "Yes" causes the IT48 farming schedule to be added to the return.

Banking / financial / insurance business and "covered person"

"Is the company carrying on banking, financial or insurance business?" This engages specialist regimes — banks (Banks Act 94 of 1990), long-term insurers (section 29A four-fund system), short-term insurers (section 28 and the ICS01 schedule). Insurance reserving for tax purposes is fundamentally different from ordinary trading companies.

"Is the Company a 'covered person' as envisaged in paragraph c(i) to (iii) in section 24JB?" This is the IFRS-fair-value tax regime. Under section 24JB, banks, branches of banks, members of banking groups under the Banks Act, and certain authorised users of an exchange must include in (or deduct from) income all amounts in respect of financial assets and liabilities measured at fair value through profit or loss under IFRS 9. The tax treatment follows the accounting treatment, so unrealised fair value gains become taxable currently — a major departure from the realisation principle that applies to ordinary taxpayers. The "paragraph c(i) to (iii)" reference is to the categories within the definition of "covered person" in section 24JB(1), which includes banks, branches and banking-group companies. Note that legislation effective for years of assessment commencing on or after 1 January 2026 narrows a previously broad exemption for dividends recognised under IFRS where these are used to hedge financial liabilities — so the section is in active flux.

Multinational enterprise (MNE)

"Is the company part of a multinational enterprise?" This question is the gateway to several heavyweight regimes:

-

Section 31 transfer pricing, which requires all cross-border related-party transactions to be priced at arm's length, with self-imposed primary and secondary adjustments where they are not.

-

Country-by-Country (CbC) reporting under section 25 of the TAA and the SARS BRS for CbC, applicable to MNE groups with consolidated turnover above R10 billion, with master file and local file requirements at lower thresholds.

-

The Coronation case (Constitutional Court, 2024) and BEPS Action Plan considerations sit behind the increased scrutiny here.

Change of financial year

"Did the financial year end change during the year of assessment?" / "Financial period used: Start / End" The "year of assessment" for a company is its financial year as defined in section 1(1) of the Act, which in turn looks to the Companies Act. A change of year-end (permitted under section 27 of the Companies Act) creates a transitional period that is not 12 months. This affects:

-

Pro-rating of capital allowances (e.g. section 12C wear-and-tear is per year of assessment);

-

Provisional tax calculations under the Fourth Schedule, including the basic amount uplift;

-

Assessed loss utilisation under section 20, including the 80%-of-taxable-income cap introduced for years of assessment ending on or after 31 March 2023;

-

Section 9D CFC inclusions, which are computed by reference to the CFC's foreign tax year ending during the resident's year of assessment.

Oil and gas

"Is the company an Oil and Gas Company as defined in the 10th schedule?" The Tenth Schedule to the Act is a self-contained regime for oil and gas exploration and production. It provides:

-

A maximum corporate tax rate (currently lower than the standard rate, depending on the operations);

-

100% upfront deduction of exploration expenditure and 50% of development expenditure in the first year, with the balance over subsequent years;

-

A fiscal stability clause allowing OP26 right-holders to bind SARS to the regime for the duration of the right;

-

Reduced withholding tax rates on dividends and interest paid offshore by oil and gas companies.

It is the most generous extractive-industries regime in the Act and is bolt-on to, rather than part of, the ordinary mining regime in sections 15, 36 and 37 read with the various capex allowances.

A practical thread runs through all these tick boxes: each "Yes" widens the return with a dedicated container or schedule, and each ticked box meaningfully shifts the legal risk profile of the assessment. Section 99 of the TAA gives SARS three years to reassess as a baseline, but prescription does not apply where the assessment was procured by fraud, misrepresentation, or non-disclosure of a material fact — and the tick-box disclosures are precisely the "material facts" SARS will point to. Getting any of them wrong (by omission as much as by overclaim) effectively opens the year up indefinitely.

Distributions from Trusts have to be shown on the screen. When adding the distributions ensure that the required detail is inserted.

26 June 2023