IT12 Trust Reportable Arrangement

If there is a reportable arrangement the following screen must be entered, otherwise don't enter.

Yes. A trust can be a “participant” in a reportable arrangement and will then have a mandatory disclosure obligation under sections 34–39 of the Tax Administration Act (TAA).

## 1) What is a “reportable arrangement” (TAA s34–36)?

- “Reportable arrangement” means an arrangement referred to in TAA s35(1) or s35(2) that is not an excluded arrangement under s36.

- “Participant” (who must disclose) includes:

- the promoter;

- a person who will (directly or indirectly) derive a tax benefit or financial benefit from the arrangement; or

- a person party to an arrangement listed by the Commissioner in a public notice under s35(2).

- A “tax benefit” is the avoidance, postponement, reduction or evasion of a liability for tax.

### When is an arrangement reportable? (TAA s35)

An arrangement is reportable if a participant is involved and it meets any of the s35(1) triggers, for example:

- fees/interest/finance costs depend (wholly/partly) on assumptions about the tax treatment of the arrangement;

- it has characteristics contemplated in ITA s80C(2)(b) (or substantially similar);

- it creates a book/tax mismatch (deduction for Income Tax but not an expense for financial reporting, or vice versa);

- it lacks a reasonable expectation of pre-tax profit, or the pre-tax profit is less than the present value of the tax benefit.

It is also reportable if the Commissioner lists it in a public notice under s35(2).

### Excluded arrangements (TAA s36)

Certain arrangements may be excluded (e.g. certain stand-alone debts, leases, regulated exchange transactions, CIS transactions), but exclusions do not apply if the arrangement is entered into mainly to obtain/enhance a tax benefit or structured to enhance a tax benefit.

## 2) Disclosure obligation and time limits (TAA s37)

- A participant must disclose the prescribed information within 45 business days:

- after the arrangement qualifies as reportable (if already a participant), or

- after becoming a participant (if joining later).

- SARS may grant an extension of a further 45 business days if reasonable grounds exist.

- A participant need not disclose if it obtains a written statement from another participant confirming that the other participant has disclosed the reportable arrangement.

## 3) What information must be submitted? (TAA s38–39)

The disclosure must include (in the prescribed form/manner and by the specified date), among other items:

- a detailed description of all steps and key features;

- a description of the assumed tax benefits;

- names/registration numbers/addresses of all participants;

- a list of agreements; and

- any financial model reflecting the projected tax treatment.

After SARS receives the information, SARS must issue a reportable arrangement reference number to each participant (for administrative purposes).

## 4) Penalties for non-disclosure (TAA s212)

If a participant/promoter fails to disclose as required by s37, SARS may impose a monthly penalty (up to 12 months):

- R50,000 per month (non-promoter participant/intermediary), or

- R100,000 per month (promoter).

This can be doubled if the anticipated tax benefit exceeds R5 million and tripled if it exceeds R10 million.

## 5) Trust return (ITR12T) – where it appears

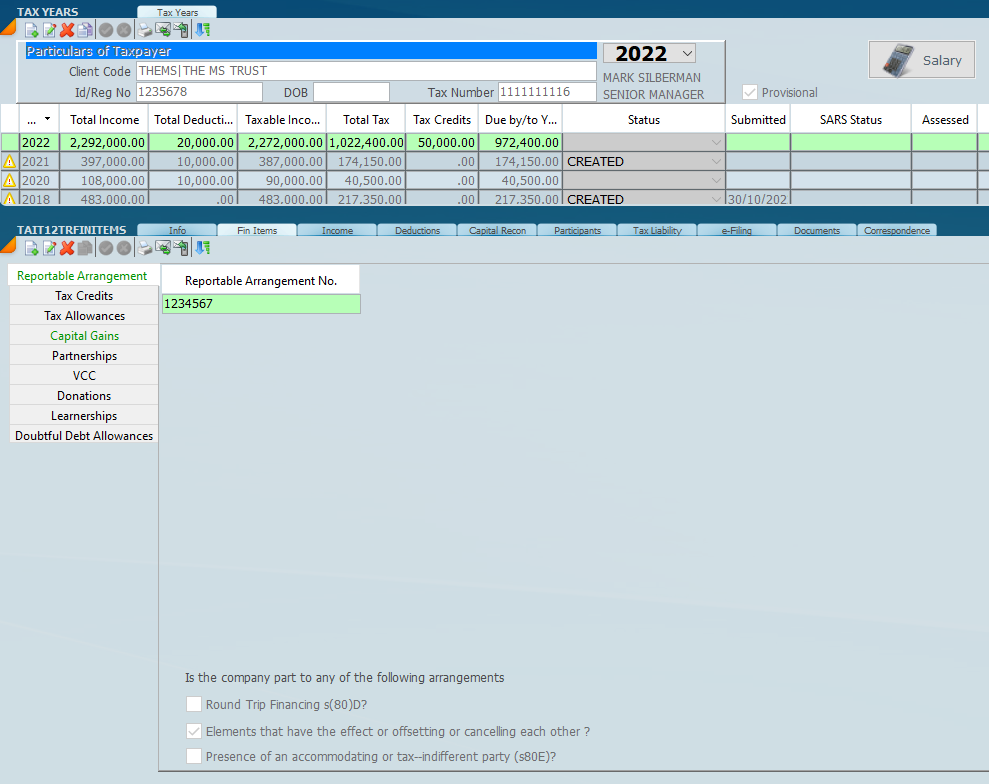

SARS’ trust return guide confirms that trusts must answer whether the trust entered into a reportable arrangement in terms of TAA ss34–39, and if “Yes” the trust must complete the “Reportable Arrangement” section and capture the reportable arrangement number/reference number issued by SARS.

The guide also flags features/questions such as round trip financing (s80D), offsetting/cancelling elements, and accommodating/tax-indifferent parties (s80E).

12 May 2026