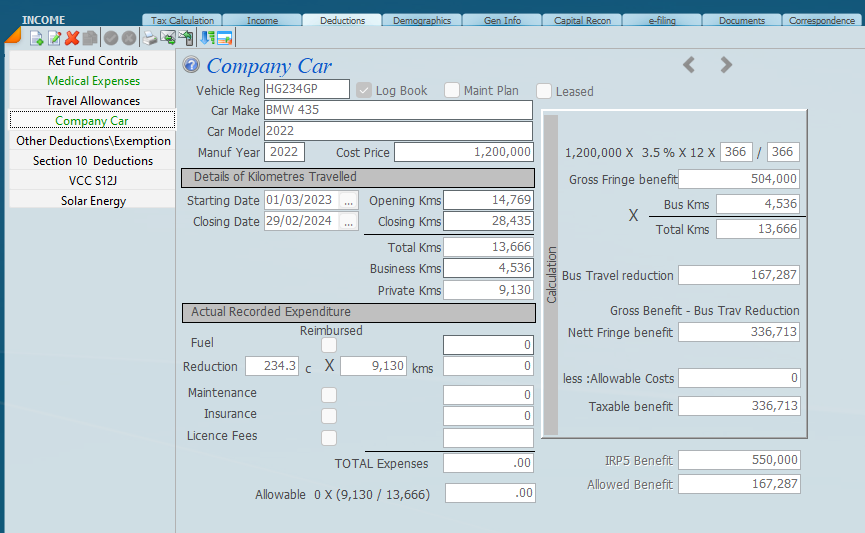

The screen below indicates the company car details. Log book details should be entered. When a new record is created the details of the car are brought forward. The source code on the IRP5 is 3802 and this amount is added to the gross income and the system works out the allowed benefit from the actual value of the car in terms of the legislation.

In the screen above the net taxable amount on the use of the car is 550,000 less 167,287.

Important Note

In many instances the fringe benefit on the IRP5 is incorrect. SARS accepts these figures but the the company in question is exposing themselves with incorrect figures especially when it is overstated. Sky calculates the fringe benefit correctly - see the top right hand corner. If the IRP5 overstates the benefit we limit it to the correct amount. If the benefit is understated we make the benefit the correct amount.

How the fringe benefit for the right to use on a car is calculated for PAYE purposes

1. Determined Value:

- If the vehicle is purchased by the employer, the determined value is the original cost excluding finance charges.

- For leased vehicles (not operating leases), the retail market value or cash value is used.

- If the vehicle was acquired more than 12 months before the employee was granted the right of use, a depreciation of 15% annually on a reducing-balance method is applied.

2. Monthly Benefit:

- For non-operating lease vehicles, 3.5% of the determined value is included as a monthly taxable benefit. This reduces to 3.25% if the vehicle was subject to a maintenance plan when acquired.

- For operating lease vehicles, the taxable benefit equals the actual lease cost plus fuel costs.

3. Reduction of the Taxable Benefit:

- Business Use: If the vehicle is used for both private and business purposes, a business use reduction is allowed. The reduction is proportional to the ratio of business kilometres to total kilometres travelled, provided accurate records (logbooks) are maintained.

- Employee-Borne Costs: An employee may claim reductions if they bear the full costs of licensing, insurance, maintenance, or fuel for private use. The reduction is calculated based on the proportion of private kilometres to total kilometres.

4. Special Circumstances:

- No taxable benefit arises if the vehicle is used as a pool car by employees in general, with private use being infrequent and incidental, or if the employee's duties regularly require after-hours use of the vehicle, with private use limited to commuting or incidental use.

5. Employers’ Tax Withholding:

- Employers must include 80% of the calculated taxable benefit in the employee's remuneration for tax purposes. If the employer is satisfied that at least 80% of the vehicle use is for business, this percentage reduces to 20%.

23 August 2025